All of us have felt the economic impact of COVID-19. The global economic pain has depressed values of businesses, stocks, real estate and most other investments. However, current low interest rates, low asset values and current tax rules related grantor trusts create a favorable estate planning environment.

Although it may be some time before the economy recovers, there appears to be a window of opportunity for estate planning.

Current estate tax exemptions of $11,580,000, which are $10 million plus inflation adjustments since 2011, will adjust back to $5 million plus inflation adjustments since 2011 in 2026. This cuts the current exemption in half (upwards of $6 million) in 2026.

The trillions spent to address the current pandemic and the upcoming November elections create concern that the current favorable estate and gift tax rules may be changed.

We understand estate planning can be difficult, because there are many tough decisions you have to make when the future is uncertain for your family.

Those fortunate enough to have taxable estates may not want to pass on all of their wealth to their children right away. Therefore, estate planning is usually a slow process, using trusts until children are fully ready for direct ownership of the wealth.

With the recent and upcoming changes, here are some estate and gift opportunities to consider:

- Use of your annual exclusion gifts of up to $15,000 per child, or $30,000 if both parents make gifts. As families grow, grandparents can shift large amounts of wealth through these annual gifts to their children and grandchildren (some individuals with large families gift more than $500,000 each year in annual exclusion gifts). As a reminder, direct payments for medical services or educational tuition for anyone, related or not, are not considered gifts.

- Large gifts of assets with depressed values. The current low values and the high individual estate, gift and generation-skipping exemption of $11,580,000 allows large current transfers to children or trusts, but this amount will be cut in half in 2026. This creates a window through 2025, unless there are earlier law changes due to COVID-19 and or political shifts, to take advantage of the $11.58 million exemption before it is reduced by upwards of $6 million.

- Making low-interest loans to children for homes or business opportunities is very attractive, as June’s Applicable Federal Rates (AFRs) are at .18% for loans three years or less, .43% for loans more than three years and not more than nine years, and 1.01% for loans more than nine years. Note Section 1274(d)(2) states that in the case of any sale or exchange (loans or IDGT sales), the AFR shall be the lowest three-month rate. This means the lowest of the rate in effect for the calendar month of the sale or exchange, or the rates in effect for the prior two calendar months. This rule does not apply to GRATs, as Section 2702 mandates the Section 7520 rate, which is different from the AFR apply for the month the GRAT is settled.

- Grantor trusts can be used to leverage high estate and gift exemptions, low asset values and low interest rates. Current grantor trust rules are the foundation for many of the most powerful estate planning strategies, but there is concern these rules could be eliminated along with other increases in estate or income taxes in the future.

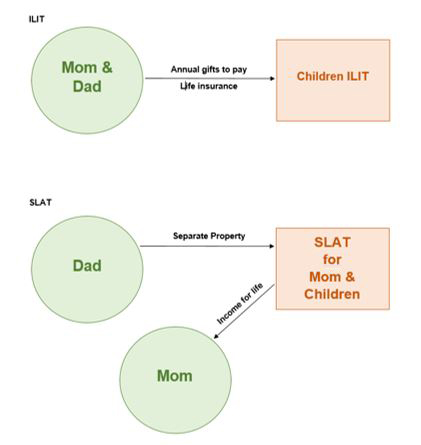

- Spousal lifetime access trust (SLAT) for a married couple takes advantage of the current high gift tax exemption amount of $11.58 million and permits your spouse continued access to the income to sustain cash flow, as shown below. Estate planning with the control of the cash flow makes this grantor trust attractive, as long as divorce or premature death are not concerns. The risk of a premature death can usually be addressed with life insurance or an irrevocable life insurance trust (ILIT). It is possible to have each spouse create a SLAT for the other spouse, but each SLAT must be substantially different assets, different trustees, different terms, and the trusts must be established at different times to avoid the Reciprocal Trust Doctrine rules, which can be achieved by planning with your estate tax advisors.

- Irrevocable life insurance trusts (ILITs) are used in conjunction with many estate planning strategies to provide liquidity and address the risks of premature death. The ILIT is typically funded using annual exclusion gifts to pay premiums on first or second-to-die life insurance policies owned by the trust that is outside the insured’s estate. The trust beneficiaries can use the life insurance proceeds to purchase estate assets and provide the estate with cash to pay estate taxes. The ILITs are used in conjunction with SLATs or GRATs, to ensure the spouse and/or beneficiaries have cash to address estate tax and other liquidity needs.

- Grantor retained annuity trusts (GRATs) are used to transfer assets from parent to child that have high potential for appreciation. Current low rates and low values make these trusts attractive and any asset appreciation over our current low values is passed on to GRAT beneficiary without a downside, i.e., if the assets fail to appreciate the entire asset comes back to the grantor. Rolling GRATs with short terms of three years or so are often used for shares of stock with an expectation of high appreciation. If the there is none, the shares come back to the grantor and are placed into a new GRAT. Note, for many years there has been proposed legislation that would outlaw short-term GRATs and require a minimum of 10-year term with a gift of at least 25%. Direct gifts, sales to IDGTs and assets funding GRATs all benefit from asset valuation discounts associated with minority ownership and lack of marketability which may apply to stock shares, interests in LLCs and partnerships and fractional interests in real property.

- Sales to intentionally defective grantor trusts (IDGTs) can be used to transfer business interests, real property and other investment assets from one generation to the next without generating income tax. The sale of assets from the parent (grantor) to a separate IDGT for the benefit of the children can be designed to complete the nontaxable sale of the assets usually over a term of 15 years or less.

The IDGT is also required to have 10% equity to help secure the note (i.e., a gift of 10% of the purchase is required). IDGTs are generally considered one of the most powerful grantor trust strategies and are effective in transferring $1 million to over $100 million between generations, depending on the type of assets being transferred. Note, sales to IDGTs are generally used to transfer assets that will be held for the foreseeable future.

This is because the assets sold to the IDGT retain a carryover tax basis from the grantor, which is usually low and does not acquire a step-up in tax basis of these assets at the grantor’s death or from the nontaxable sale to the IDGT. Sales to IDGTs avoid the estate tax, but if these assets are sold soon after death, their low income tax basis creates high income taxes. This offsets most of the estate tax benefits. The current low interest rates and low asset values, make sales to an IDGT a particularly powerful strategy to be considered in your estate planning.

Sales to IDGTs should also consider using self-canceling installment notes (SCINs), which increase the sales price or increase the interest rate on the note. Also, the premium paid provides for a cancellation-at-death feature in the note. SCIN rates seem more reasonable given the current low AFRs and should be considered for individuals generally age 70 or younger. SCINs should not be used with notes that extend past the individual’s expected lifetime. Note, some planners include a SCIN with a regular note on the same transaction to capture the benefits on a portion of the deal. Some sample premiums for a 10-year, interest only note, paid quarterly, with the June long-term AFR of 1.01% for a single life individual age 55, 60, 65 and 70, are 2.04%, 2.58%. 3.41%, and 4.82% respectively per Number Cruncher software.

- Spousal lifetime access trust (SLAT) for a married couple takes advantage of the current high gift tax exemption amount of $11.58 million and permits your spouse continued access to the income to sustain cash flow, as shown below. Estate planning with the control of the cash flow makes this grantor trust attractive, as long as divorce or premature death are not concerns. The risk of a premature death can usually be addressed with life insurance or an irrevocable life insurance trust (ILIT). It is possible to have each spouse create a SLAT for the other spouse, but each SLAT must be substantially different assets, different trustees, different terms, and the trusts must be established at different times to avoid the Reciprocal Trust Doctrine rules, which can be achieved by planning with your estate tax advisors.

-

Late allocations of Generation Skipping Tax (GST) exemption to trusts are available for trusts established years ago when the exemptions level were much smaller.

-

Consider donation of IRA to charity. When there is a taxable estate and individuals are philanthropically inclined, individuals should consider designating charities as the beneficiaries of the taxable IRAs or retirement accounts. In taxable estates, the individual beneficiaries will only receive about 25 cents on the dollar after estate tax and the individual income taxes are paid, versus the charity, which will enjoy the every cent on the dollar.

-

Payment of gift tax on taxable gifts that exceed the $11.58 million is computed at a lower effective rate of 28.57% versus the estate tax rate of 40%, and the donor must live for three years after making the gift. However, accelerating the tax is almost never used unless it is part of another planning strategy like the IDGT, etc.

-

Roth IRA conversions are drawing lots of interest with lower stock values. Having cash outside the IRA to pay income taxes and allow the IRA to rollover the entire amount to the Roth is critical. From the estate planning perspective, the Roth IRA conversions require cash, as do GRATs and sales to IDGTs. Some estates need to prioritize their estate planning strategies when cash is limited.

Economic swings and political shifts may change the estate planning landscape in the near future, and the changes may be dramatic. Now is time to get in touch with your BPM tax and estate tax advisors to plan for your family.

For more information, contact BPM Tax Partner Joseph Kitts and BPM Tax Director Sachi Danish.