INSIGHT

New Pay Versus Performance Rules to Prepare for in the 2023 Proxy Season

Kemp Moyer • January 25, 2023

Rules target relationship between executive compensation and financial performance

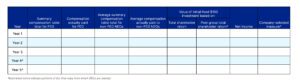

In August 2022, the Securities and Exchange Commission (“SEC”) adopted rules requiring registrants to disclose the relationship between executive compensation paid and the financial performance of the company. The new rules require additional disclosures in annual proxy statements for fiscal years ending on or after December 16, 2022. The required reporting consists of a table (see below) that provides specified executive compensation and financial performance measures for the five most recent fiscal years (smaller reporting companies can submit three years), as well as a narrative that illustrates the company’s relationship between executive compensation and performance.

Under the rules and as shown in the table above, disclosures are required for the registrant’s principal executive officer (“PEO”) as well as other named executive officers (“NEOs”) besides the PEO. Smaller reporting companies (“SRCs”) are exempt from certain requirements.

In the initial year of adoption, only three years of information must be provided, with an additional year added in each of the two subsequent proxy filings. Smaller reporting companies may provide two years in the initial year, with the third year added in the subsequent year. These rules apply to all SEC reporting companies except for foreign private issuers, registered investment companies and emerging growth companies.

Other financial performance measures required in the table include:

-

- Total shareholder return (“TSR”) for the registrant;

- TSR for the registrant’s peer group;

- The registrant’s net income; and

- A financial performance measure chosen by the registrant (the “Company-Selected Measure”) that, in the registrant’s view, represents the most important financial performance measure the company uses to link compensation actually paid to the registrant’s NEOs to company performance for the most recently completed fiscal year.

These new SEC rules are complex and certain data, including newly required compensation calculations (e.g., the new concept of executive compensation “actually paid”), will require companies to expend significant resources on compliance. Most companies will need to provide the “pay versus performance” disclosures in their upcoming 2023 proxy statement and most of the initial disclosures will require information for the previous three years.

BPM Can Help

Companies should already be coordinating efforts with key internal departments (e.g., finance/accounting, legal, human resources, investor relations and public relations) and outside advisers (e.g., BPM’s compensation consultants and valuation experts, as well as legal counsel). Many of the required “pay versus performance” calculations are likely to be time-intensive, particularly with respect to stock options and market-based performance awards. The rules also make the determination of an accurate peer group set more important than ever before. BPM can help.

To facilitate “pay versus performance” compliance, BPM’s experienced financial analysis professionals work with companies to develop a comprehensive benchmarking strategy and identify key financial metrics to help determine the appropriate peer group set. This analysis also identifies the financial metrics that best relay the narrative of how and why company executives are compensated.

With the new SEC reporting requirements placing increased scrutiny on compensation structures, as well as a challenging market environment putting pressure on a variety of reporting requirements and board decisions, BPM understands sage guidance is more critical than ever. Our team provides independent third-party support that can help with navigating both proxy season and audit processes. BPM’s seasoned professionals can help guide companies through the new requirements and provide peace of mind for executives, boards and auditors.

To learn more about our services or for questions about the SEC’s Pay Versus Performance requirements, contact Kemp Moyer or Jean Chen.

Start the conversation

Looking for a team who understands where you’re headed and how to help you get there? Whether you’re building something new, managing growth or preserving success, let’s talk.