INSIGHT

Inflation Shocks are Hitting Consumer Businesses From All Sides

Dylan Mead, Megan Lombardi, Ryan Musser • January 18, 2023

Elevated inflation levels and a potential recession may force consumer businesses to shift their priorities in 2023 as their customers’ capacity for spending diminishes.

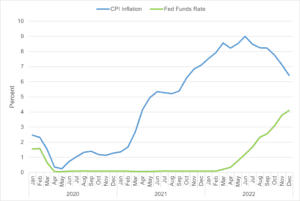

High inflation, rising interest rates and market volatility have plagued the U.S. economy for months. As a result, many businesses are foreseeing higher borrowing costs, softening growth and other gloomy projections for the year ahead. Specifically, inflation began to rise above the U.S. Federal Reserve’s 2% target in early 2021, peaking at 9.1% in June 2022. In response, the Fed has aggressively hiked interest rates with the goal of cooling the economy off to get inflation down. As illustrated in Figure 1 below, that strategy — for now — appears to be working.

Now that inflation has started to move in the right direction, the expectation is that the Fed will likely adopt a less aggressive rate hike schedule going forward as it balances the need to lower inflation against recession risks. However, given the fact that inflation remains far above the Fed’s 2% target, additional rate hikes are still anticipated.

Emerging Consumer Challenges

The U.S. consumer has remained fairly resilient in 2022 despite the day-to-day impacts of high inflation. However, two significant trends are emerging that could be a harbinger of more challenging times ahead.

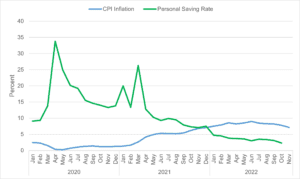

1. Falling savings levels: The payments issued by the federal government in response to the global pandemic helped to boost personal saving rates temporarily. But as inflation increased — and prices on items such as food and housing spiked — those funds have dwindled. This means that many consumers now have (or will soon have) less capacity for discretionary spending.

2. Increasing debt levels: Credit card debt bumped up in 2019 and early 2020, then plummeted through 2020, likely because of impacts from federal stimulus programs. However, in 2022, we’re seeing credit card debt climbing in lockstep with inflation. This supports the idea that consumers are starting to stretch beyond their means to keep up with purchases that are getting increasingly expensive.

Impacts on Consumer Businesses

While consumers themselves are starting to feel the impacts of inflation in their bank accounts and credit card statements, businesses in the consumer sector have been grappling with a long list of their own pressures in the current economic environment, including:

- High labor costs: The labor market remains relatively tight, and competition for talent continues to be strong (although the employment picture is starting to show signs of easing). In the meantime, companies are balancing recessionary impacts against offering competitive compensation to hire and retain employees.

- Increased cost of borrowing: As the Fed continues to raise interest rates, the cost of capital has become prohibitive in many cases. This is forcing companies that may be short on funding to figure out how to stay operational through other means such as cutting headcount and costs instead of turning to borrowing.

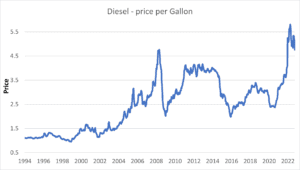

- Rising energy costs: Energy prices have soared due to inflation, strong demand and the war in Ukraine. As a result, many companies are searching for ways to reduce energy consumption across their supply chains.

- Inventory backlogs: Many well-known retailers have reported inventories that dwarf the previous years’ levels. Consumer businesses that acquired this excess inventory at already high prices may find it more difficult to pass price increases to their increasingly cash-strapped customers and will likely need to consider sales and discounts. Further, there are often additional costs associated with the storage of surplus products — another potential drag on profits.

How BPM Can Help

High inflation is impacting all sectors, but the crisis is playing out daily and acutely in the consumer sector — for consumers themselves and for the retailers that serve them. On the individual level, purchasing power is starting to weaken as excess cash dries up and credit card debt inches upward. Meanwhile, consumer businesses are grappling with rising costs across their operations and limited borrowing power in a rising rate environment. These pressures will likely cause many consumer businesses to shift their focus from market-share growth and customer experience to pure capital management and maintenance of margin performance. The bottom line is that 2023 will likely be a challenging year for both retailers and their customers.

Our experienced professionals can help you minimize uncertainty in the current market environment in a number of ways, including:

- Harnessing predictive analytics to provide insight into the future of your business and the economy.

- Maintaining visibility into finances and resources with custom-built dashboards.

- Maximizing customer engagement and marketing spending with customer intelligence.

- Optimizing your labor force by automating repetitive or time-intensive tasks.

Start the conversation

Looking for a team who understands where you’re headed and how to help you get there? Whether you’re building something new, managing growth or preserving success, let’s talk.