INSIGHT

How to Navigate Increasing IRS Enforcement

March 3, 2022

IRS tax enforcement is on the rise and small errors could lead to big penalties and even charges of tax evasion. Learn how to avoid mistakes, what to do if you make one, and who to call to avoid this sort of trouble.

By Fred Chang, International Tax Director

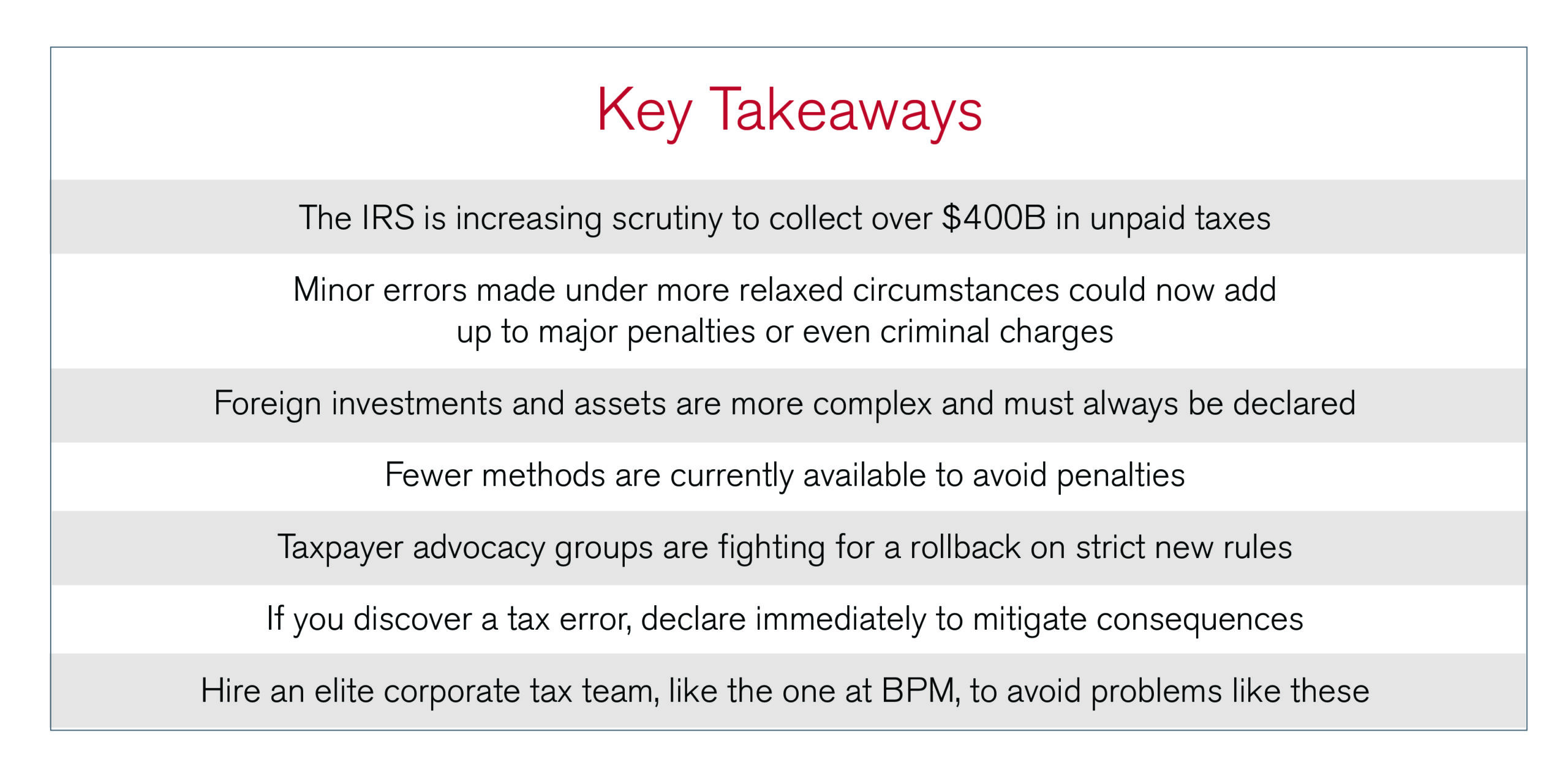

Taxes are inevitable. However, specific policies and how strictly they are enforced can vary wildly by administration and can even change from month to month. When enforcement is relaxed, errors or omissions can repeat, unnoticed, for several years. Then, when vigilance increases, the IRS goes through prior records and finds duplicate irregularities. Suddenly businesses face several years’ worth of arrears, mounting penalties and even potential criminal charges when for some time neither the taxpayer nor the tax collectors even realized any mistakes had been made. Stir in the complexities of overseas holdings, and you have a recipe for a fiscal and legal disaster.

Recent trends have pointed to tax enforcement becoming stricter, with new forms required and rules to obey, as well as renewed scrutiny for outstanding errors. At BPM, we’ve seen an influx of businesses and accountants alike reaching out about notices from the IRS regarding unfiled forms, outstanding taxes, and hefty penalties on both. As accountants ourselves, we have investigated similar stories from friends and peers. These fact-finding exercises reveal that many individuals and companies are unaware of all the extensive filing requirements they must fulfill, despite being eager to learn and keep business running smoothly.

International Tax

Filing taxes is complicated enough when a business is solely domestic. For firms with multinational or international operations, the learning curve is steeper. One major misconception among business owners is that there is no need to report the start of a new business in a foreign country when that business has yet to generate any notable activity.

The reality is that any business activity in a foreign country could introduce an additional filing requirement. Companies that fail to report a foreign operation can be subject to monetary penalties of $10,000 per missed filing, which can grow to be even more significant if the failures stack up for a number of years. As markets globalize, the IRS is becoming more vigilant for outstanding errors like these, where before companies might have skated by in ignorance of the rules.

IRS Enforcement

IRS vigilance is increasing across the board. In late 2021, Deputy Treasury Secretary Adeyemo announced plans to collect $400 billion in unpaid taxes, both to fund government projects and to use fear of audits to deter tax avoidance.

As part of this initiative, the IRS is issuing automatic notices to business owners whose tax payments have been light or who have foreign bank accounts or investments. Any number of discrepancies could raise a red flag among tax collectors. This “shoot first, ask questions later” approach to enforcement lets the department cast a wide net as they recoup outstanding funds, putting the onus on taxpayers to prove themselves innocent.

All over the country, notices are going out, informing companies of missing filings and penalty bills for tens of thousands of dollars. Business owners leave these discrepancies to their tax advisors to sort out, with few options but to seek a reasonable cause exception.

But the standards to qualify for Penalty Relief Due to Reasonable Cause are quite high and, as with many legal matters, ignorance is no excuse. No matter how fast standards change or how obscure the tax codes are that slipped through the cracks, the IRS expects organizations to pay every penny they owe.

Voluntary Disclosure Practice

It is important to realize that this new rigor can land companies in hot water. IRS personnel understand that many of these missing payments are due to human error and not to tax fraud. To this end, the IRS offers initiatives like the Voluntary Disclosure Practice that takes into account the taxpayer’s overall history of disclosure to determine whether to pursue criminal charges. Unfortunately, a similar offering for international assets, the Offshore Voluntary Disclosure Program, is now defunct, increasing the risk of costly errors by multinational companies.

Even without an applicable program available to cover their specific lapse, companies are best advised to come clean to the IRS as soon and as completely as possible. An amended return, a sincere mea culpa and a reasonable cause statement can potentially help avoid significant penalties and other significant detriments. Paying the final assessed penalties in good time also helps. Clients in this situation ask if they’re better served to admit their mistake or let the IRS figure it out for themselves, and the answer is always the former. There is no guaranteed safe harbor in the case of unpaid taxes, and no explicit guidance on gaining leniency.

Avoid the Problem

Of course, the very best way to avoid these penalties and potential legal repercussions is to respond to increased scrutiny with increased care. If you’re planning to expand your business outside the United States, learn about and be sure to meet any new or obscure requirements.

This is especially true for owners of small- to mid-sized businesses. The largest firms already have top in-house finance departments, strong relationships in government and enough money to pay any fines. Smaller enterprises are both more vulnerable to mistakes like this and face more serious risks if discovered.

Leaders looking to avoid this sort of trouble should retain a finance team, like the BPM Corporate Tax Services team or International Tax Services team, that will practice all possible rigor to protect their clients against simple mistakes that could lead to complex problems. With tax codes and collector scrutiny changing all the time, the best defense against unforeseen penalties is an elite finance team to do the foreseeing for you.

Key Takeaways

Subscribe to Our Thought Leadership

Found this article helpful or interesting Sign up now for periodic industry news and insights curated by BPM thought leaders, sent directly to your inbox. In the meantime, feel free to share this article with peers and colleagues using the buttons below.

Start the conversation

Looking for a team who understands where you’re headed and how to help you get there? Whether you’re building something new, managing growth or preserving success, let’s talk.