INSIGHT

Business Valuation for Divorce Purposes

July 7, 2023

Divorce and business valuation matters can be challenging and sensitive. Add in the dynamics of closely held business and the division of property can quickly become a highly contested issue. When less clearly defined business ownership interests are included in the process, the parties involved will often disagree over the value of such interests, often necessitating the need for an objective expert valuation of the business. Unfortunately, the valuation exercise is further complicated by jurisdictional statutes and case law precedents that determine the applicable standard of value and how personal goodwill should be treated (or not). When such situations do arise, it is essential to work with a business valuation expert who understands these legal nuances and can provide an objective and accurate assessment of the business’s worth. This approach can help ensure that the division of assets is fair and equitable, despite the complexities of the legal requirements.

Divorce Business Valuation Standard of Value

When it comes to the standards of value to be used in business valuations, few areas of law are as ambiguous and inconsistent as the family law arena. The standard of value is almost never properly defined in the family law statutes. Rather, the definition of value is commonly established by a thorough review of case law and precedent. Even when a standard of value is defined, prior court decisions appear to interpret the standard of value differently depending on case specifics.

The most commonly used standards of value are defined as follows.

Fair market value: Typically defined as the price at which property would change hands between a willing buyer and a willing seller when the former is not under any compulsion to buy and the latter is not under any compulsion to sell, both parties having reasonable knowledge of the relevant facts.[1] Application of fair market value generally focuses on what elements of business value are considered transferable, or the value in exchange premise of value.

Fair value: This term in this situation may differ from the “Fair Value” term defined for GAAP financial reporting standards under FASB. Within this particular context, it is typically defined in connection with dissenting shareholder and oppression cases in the corporation statutes and established by case law precedent. Overly simplified, fair value can be viewed as fair market value without discounts for lack of control or marketability incorporated into the analysis. The attorney involved should ensure that fair value is applied appropriately based on the appropriate premise of value: value in exchange or value to the holder.

Investment value: Typically defined as the value to a particular investor based on individual investment requirements and expectations. “Investment value,” also known as “intrinsic value” or “value to the owner,” is generally developed without consideration of discounts for lack of control or marketability, as such value does not contemplate a hypothetical or actual sale of the business.

A high-level summary of the standard of value to be applied by state is presented in the table below.

Treatment of Personal Goodwill in Divorce Valuations

When determining what qualifies as marital assets, the matter of goodwill is frequently raised and closely linked to the standard of value. So, what is personal goodwill, and is it considered a marital asset? To answer this question, let’s first define goodwill.

The IRS defines goodwill as “…the value of a trade or business attributable to the expectancy of continued customer patronage. This expectancy may be due to the name or reputation of a trade or business or any other factor.”[2]

Goodwill is defined in the International Glossary of Business Valuation Terms as: “An intangible asset which represents any future economic benefit arising from a business or a group of assets which is not individually identified or separately recognized. Goodwill can arise as a result of name, reputation, customer loyalty, location, products, and similar factors not separately identified. that arises as a result of name, reputation, customer loyalty, location, and similar factors not separately identified.”[3]

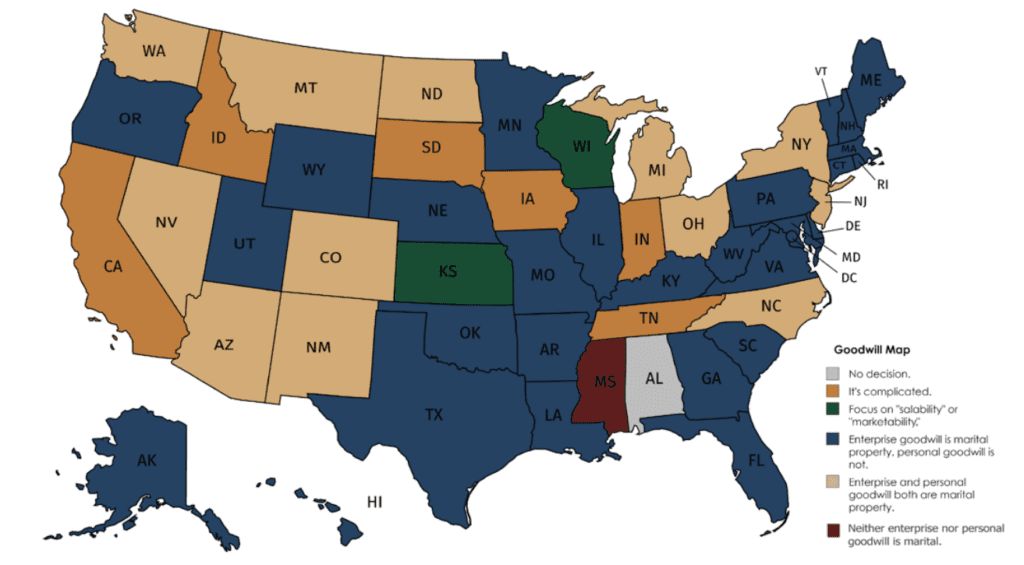

With these definitions established, we can now focus on the ‘personal goodwill’ aspect of goodwill. Goodwill can be categorized into two parts: personal (or professional) goodwill and enterprise (or commercial) goodwill. Personal goodwill can be considered goodwill that is attributable to the skills, abilities and reputation of an individual or group of individuals. In contrast, enterprise goodwill refers to goodwill that is linked to the business itself, regardless of the individuals. The distinction between personal goodwill and enterprise goodwill can be challenging to discern, and the legal treatment of goodwill varies by state. In some states, personal goodwill is considered a marital asset subject to division; in others, it is deemed separate property.

For example, in California, personal goodwill is considered a marital asset. In Texas, however, personal goodwill is regarded as separate property as such value cannot be divided and is attached to the individual upon divorce. Consequently, business valuation experts handling divorces in these states must differentiate between enterprise and personal goodwill. This can be a particularly contentious and confusing area in divorce cases, especially when a divorcing spouse owns and operates a professional practice.

A state-by-state breakdown of goodwill jurisprudence,[4] prepared by Business Valuation Resources, is presented below:

Many factors affect personal goodwill and enterprise goodwill. In evaluating whether personal goodwill exists, the following questions and factors[5] should be considered:

- Earning power: Are normal earnings expected? If there are greater than normal earnings, are they obtained through goodwill?

- Reputation: Does the professional have a reputation in the community for judgment, skill and knowledge?

- Age and health: Is the professional relatively young and still in good health? If so, there will typically be more goodwill established.

- Work habits: Is the professional hardworking, diligent and conscientious?

- Duration of business: How long has it existed?

- Referrals diversity: Does one person at the company bring in all referrals?

- Location: Is the business in a prime location that more easily attracts clients?

- Size of business: Is the business relatively simple and operating under a sole practitioner? Or is it complex, larger and has multiple revenue generators? Typically, as a company increases in size and complexity, goodwill can transition from being primarily personal to mostly entity-related.

- Source of new clients: Are clients coming in because of the professional and their relationship to the business?

- Compensation: Is the professional’s income in an average range?

- Size of workforce: Is the workforce large or highly skilled, thus adding value to the entity?

- Competition: Does the entity have lots of competition, or does it “own” its market?

Putting It All Together

In the context of business valuation and divorce, it is imperative that the business valuation expert and attorney agree early on as to the appropriate standard of value to be applied and whether personal goodwill is to be considered part of the marital assets at stake. To ensure a fair outcome in cases of marital dissolution, it is advisable to enlist the services of a qualified valuation professional who can leverage their expertise, knowledge and learned real-world experience.

The Goal is Resolution

Need to resolve a complex valuation dispute? Unwind a marriage with business ownership interest assets? Distinguish personal goodwill from enterprise goodwill? BPM’s knowledge and experience in valuation, mediated settlements and litigation support help our clients to attain fair settlements and positive outcomes — while controlling legal costs.

[1] Estate Tax Regulations § 20.2031-1.

[2] IRS Regs. Sec. 1.197-2(b)(1)

[3] https://www.appraisers.org/docs/default-source/5—standards/revised-bv-standards-february-2022.pdf?sfvrsn=d5b561b2_12

[4] https://sub.bvresources.com/FreeDownloads/ChartingGoodwill.pdf

[5] The Handbook of Divorce Valuations,” Robert E. Keeman, R. James Alerding and Benjamin D. Miller, September 1999

Start the conversation

Looking for a team who understands where you’re headed and how to help you get there? Whether you’re building something new, managing growth or preserving success, let’s talk.