INSIGHT

Assessing the Commercial Real Estate Market Amid Today’s Economic and Banking Conditions

Mark Leverette • April 20, 2023

Services: Outsourced Accounting

What’s top of mind for real estate financial leadership

As part of her prepared remarks to the National Association for Business Economics (NABE), United States Treasury Secretary Janet Yellen recently suggested that the U.S. government should strengthen its banking rules, or at least enforce them more completely on more banks. In related remarks at a recent press conference, Federal Reserve Chair Jerome Powell similarly indicated the board was assessing the right policies to put in place, so that it doesn’t happen again, then implementing those policies.

Meanwhile, entrepreneur and investor Mark Cuban shared his gut reaction on his Twitter account and in subsequent interviews, suggesting that opening many more accounts for his companies as a measure to insure more funds below the Federal Deposit Insurance Corporation (FDIC) limit. This didn’t account for the tag-on accounting requirements of increased bank reconciliations, added treasury oversight, layers of internal controls and overall additional overhead required. Cuban later noted the goal of added insurance, regardless of where it comes from, will add associated premiums that are acceptable and necessary.

To adapt to these changes, finance functions need to revise their treasury management strategies and processes, and that may involve:

- Revising investment policies.

- Implementing new cash management tools.

- Renegotiating banking relationships to ensure adequate access to credit and other services.

With the highlighted risks to our banking institutions, management and finance functions should be aware of the hazards associated with losing lines of credit they had planned to use for normal operations or strategic plans.

Additionally, derivatives, such as rate caps and swaps, have increased counterparty risk. As a result, companies should work closely with their banks and other service providers to analyze their risk exposure while they optimize their treasury operations.

What Real Estate Leaders are Discussing

Today’s real estate business leaders are exposed to rapidly changing conditions related to leases, occupancy rates and increased lending limitations. Seeking to validate these insights, BPM recently convened a panel of real estate CFOs to highlight what executives are seeing in this critical sector. Related analysis and commentary are provided in the discussions that follow.

Please note that the following anonymized panel comments have been edited for length and clarity.

Treasury Management Changes

The real estate panel’s treasury management discussions identified a key takeaway: Treasurers must stay up to date on the latest developments in the banking industry and financial markets, and they should work closely with their banks and other service providers to manage risks and optimize their treasury operations. Additional commentary focused on the following:

- “We did not want to be the one that ran on the bank, so I was trying to move quickly to ensure FDIC insurance at my bank. Inevitably we needed to start some new relationships.”

- “Moving money can be difficult with multiple entities. You can get into a real mess by co-mingling funds… usually not agreeable with our operating agreements.”

- “It will be more difficult to negotiate with our banks as they are further squeezed but also as ‘too big to fail banks’ gain more power.”

Emerging Trends in Real Estate Finance

In response to continued tightening in lending standards, investment strategies in commercial office real estate finance are evolving. One trend is the rise of non-traditional lenders, such as private equity firms and hedge funds, who are increasingly investing in commercial office properties through “debt funds,” but with a low-risk tolerance that leads to a low loan-to-value (LTV) ratio. Additional trend analysis commentary focused on the following:

- “The problem with ‘debt funds’ is they have to charge such exorbitant interest rates to make sense in this market. It seems that they don’t want to take on that risk profile in their fund now due to uncertainties regarding where the rates are going.”

- “Is anybody using General Partner Capital Lines? We are seeing rates rachet up a lot – Prime plus 150bp is what to expect.”

Capital Markets and Investor Relations

The group noted there is growing interest in environmental, social and governance (ESG) investing, which seeks to align financial returns with positive social and environmental outcomes – particularly in the Euro and pension fund investor communities. Additional ESG-related assessments included:

- “Making strides forward in your companies is important.”

- “Start to put in programs and celebrate what you are already doing well.”

- “This will turn into a full-on ESG Program at some point soon – especially in the bigger real estate companies.”

Other observations highlighted skyrocketing insurance costs, with a 50% increase in earthquake coverage noted by one attendee and an instance of one nonprofit declining fire coverage rather than face an astronomical premium.

The Economic Crystal Ball

Setting aside risk management and mitigation trends, the panel members shared the following observations and forecasts regarding interest rate and credit risk areas:

- “Economists are forecasting one, maybe two more rate increases of 25 basis points, then the recession will start by the end of this year or begin early next year….”

- “…Then, the Fed will aggressively go 275 basis points down at that point next year to stabilize…”

- “…This is a frustrating forecast because it makes people sit on their hands.”

Office Debt

There was a sense that return-to-office momentum may be “too late” for some landlords. For example, recent San Francisco Bay Area media coverage indicated some eye-opening return-to-office trends among polled local employers, including the following:

- 23% of employers approximate in-office employee attendance to be three days per week.

- A smaller number, 19%, are running with worker attendance fully on premises.

- Perhaps more daunting for commercial landlords, 21% of employers are operating on a fully remote model. Further, in-office employee presence is estimated at one or two days per week by 26% of employers.

Related panel discussion regarding office debt focused on the following:

- “The Feds are watching banks so closely, especially after the last few weeks.”

- “A senior banker I know is going through an Office of the Comptroller of the Currency (OCC) exam now, and they are being asked new and super-detailed questions on their portfolio, especially as it relates to risk rating.”

- “I suspect a number of office buildings are being downgraded (akin to mark to market internally), thus resulting in margin calls if there are ongoing covenants, but certainly when it comes time to refinance.”

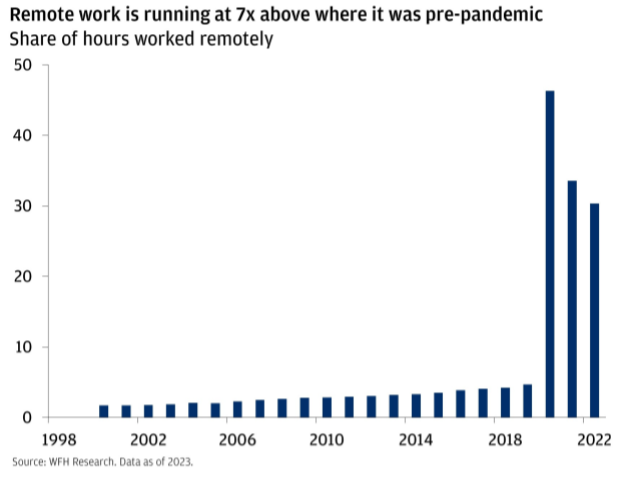

Once relegated to the likes of the cult comedy movie Office Space, WFH Research shows many employees have just stopped physically showing up at the office.

With fewer employees heading to work in person, businesses seem less inclined to rent as much office space. Vacancies in U.S. office real estate have risen in recent years, and currently sit around 12.5%, which is comparable to levels seen in the wake of the 2007-2008 Global Financial Crisis.

Combine less demand with the prospects for more expensive financing in today’s elevated interest rate environment, and the outlook for the office sector is challenged.

Too Much to Borrow

Today’s interest rates are at near-decade highs, making the cost of borrowing more expensive than it’s been in a long while. Most real estate is financed by debt, and in a space like commercial real estate – where properties tend to be leased out – the cost of servicing that debt is offset by operating income. As mentioned before, demand for office space, in particular, seems to be waning, and higher interest rates mean an elevated cost of carrying these buildings. Together, these dynamics conspire to erode the value of the property.

The worry? Property owners or managers may decide that the economics of holding onto buildings doesn’t make sense anymore (or is unfeasible). The lenders who made the loans to finance the properties in the first place could be left holding the bag.

But lenders might not be so inclined to take the keys to the building back from the borrower – it’s not exactly easy to operate, let alone liquidate, a big building on a city block. Instead of foreclosing, we think it’s likely that lenders and borrowers will come to the table to agree on loan extension options, discounted payoff plans or other means of restructuring their agreements.

BPM Summary Guidance

Real estate CFOs need to be prepared to adapt their treasury management strategies and processes to manage risks and ensure adequate access to credit and other services. By doing so, they can minimize the impact of any future banking collapses or disruptions to their operations.

Be nimble in your approach to discussions with banks about lending requirements and strategies for navigating interest rate fluctuations. As the market finds an equilibrium, those with the right toolbox will see many more opportunities.

References:

Yellen says US bank rules may be too loose, need to be re-examined

Silicon Valley Bank leaders “failed badly,” Fed Chair Jerome Powell says

‘It’s Not the Wealthy Taking the Hit’: Mark Cuban’s ‘Baby’ Among Companies With Millions In Silicon Valley Bank

Mark Leverette

Partner, Assurance and Advisory

Outsourced Accounting Leader

Real Estate Leader

Mark has devoted 20 years of experience to entrepreneurial companies. As the Managing Partner of Client Accounting and Advisory Services …

Start the conversation

Looking for a team who understands where you’re headed and how to help you get there? Whether you’re building something new, managing growth or preserving success, let’s talk.